Serving the Bay Area & Sillicon Valley

Foundation and Approach

Educated at San José State University and supported by professional designations including Certified General Appraiser, CVA, and ASA, this work reflects a combination of analytical training and decades of valuation practice.

Early experience in systems analysis and software engineering at Lockheed Missiles & Space Company established a structured, problem-solving approach that continues to guide valuation analysis across business enterprises, commercial real estate, and ownership interests.

The work integrates how value is formed in real transactions with how it must be supported under scrutiny—particularly in matters involving ownership transfer, financial reporting, and tax-related valuation.

Business Enterprise Valuation

Valuation of operating businesses where value is influenced by structure, control, and economic performance. Assignments include closely held companies, internal transactions, ownership transitions, and selected startup companies where valuation extends beyond standardized frameworks.

Analysis may include intangible assets and intellectual property, as well as valuation considerations arising in mergers, acquisitions, and related transaction structures. The focus remains on how enterprise value is formed, allocated, and supported under varying ownership and capital conditions.

Work is performed in accordance with recognized professional standards, including USPAP, and is prepared to support conclusions under review in financial reporting, tax, and transaction-related contexts. Engagements are selective and principal-led, based on the complexity of the valuation problem rather than routine or high-volume reporting.

Ownership Interests

Valuation of partial interests in entities where value is influenced by control, marketability, and structural characteristics.

Assignments commonly involve holding companies, layered ownership arrangements, and internal transfers where valuation must reflect the economic realities of ownership—not just underlying assets.

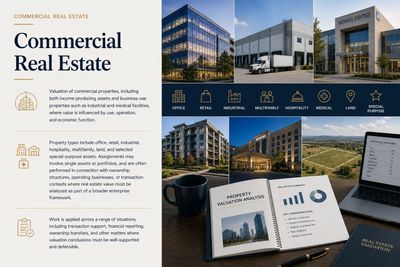

Commercial Real Estate Appraisal

Valuation of commercial properties, including both income-producing assets and business-use properties such as industrial and medical facilities, where value is influenced by use, operation, and economic function.

Property types include office, retail, industrial, hospitality, multifamily, land, and selected special-purpose assets. Assignments may involve single assets or portfolios, and are often performed in connection with ownership structures, operating businesses, or transaction contexts where real estate value must be analyzed as part of a broader enterprise framework.

Work is applied across a range of situations, including transaction support, financial reporting, ownership transfers, and other matters where valuation conclusions must be well-supported and defensible.

ESTATE AND GIFT TAX VALUATION

Valuation of closely held business interests, ownership interests, commercial real estate, and other assets in connection with estate and gift tax planning and reporting.

Assignments may involve family limited partnerships, limited liability companies, holding companies, partial interests, and underlying real estate or business assets where fair market value must be clearly supported.

Analysis may include discounts for lack of control and lack of marketability, with documentation prepared to support valuation conclusions under IRS review and related advisor coordination.

Cost Segregation Study

Engineering-based cost segregation studies for commercial real estate, identifying components eligible for accelerated depreciation under current tax law.

With the restoration of 100% bonus depreciation for qualifying property placed in service after January 19, 2025, and expanded treatment of qualified production property under Section 168(n), cost segregation continues to provide significant timing benefits for capital recovery.

Analysis focuses on proper classification of assets into shorter recovery periods (e.g., 5, 7, and 15 years), supported by documentation prepared to withstand IRS review and coordination with tax advisors.

QUALIFICATIONS OF PRINCIPAL

David Hahn, ASA, CVA, MAFF, CM&AA, CCIM, MBA

David Hahn, CVA, MAFF, ASA, CM&AA, CCIM, MBA, has been in Commercial Real Estate Appraisal, Cost Segregation Study, Business Financial Valuation, Purchase Price Allocation Study and valuation appraisal practices since 1985. The firm provides solutions for, and in tandem with, Attorneys, CPA's, Financial Advisory Groups, Governments, Lending Institutions, Corporations, Individuals and others within the realms of Intellectual Property, Trust & Estate and Business Transfers and M&A along with others requiring valuation solutions.

· State Certified General Real Estate Appraiser: CA, OR, NV, WA

· California DRE Broker #00902122

· Certified Business Valuation Analyst (CVA) credential from the NACVA

· Accredited Senior Appraiser designation of the American Society of Appraisers (ASA)

· Certified Merger & Acquisition Advisor (CM&AA)

· Certified Commercial Investment Member (CCIM), known as the Ph.D of commercial investment real estate

· College Instructor's Credential - Business & Real Estate Instructor Certified through THE TRAIN THE TRAINER program - CCIM Institute

· Taught USPAP, Commercial & Business Appraisals, Financing, Commercial Investment, more than 5,000 classroom hours since 1985.

· Competent Toastmaster (CTM) certificate from Toastmasters International

· B.S. in Industrial Technology/Computer Science, Minor in Business - San Jose State University - 1981

· Control Data Corporation, San Jose, Business Systems Analyst, 1981-1983

· Lockheed Missiles and Space Company, Systems Analyst, 1983-1985

· Executive MBA - 1983

· USC, Public enterprise cost/benefit analysis graduate course, 1993

. UCLA Executive Management Program certificate - 1995

· Doctoral Studies, Public Administration, University of La Verne, 1995-1998

. U.S. Army veteran - active duty for 3 years - honorable discharge, 1979

DAVID HAHN QUALIFICATIONS